The question in front of economic developers, manufacturers, and utilities right now is not whether to engage with the AI infrastructure buildout. That ship has sailed. The real question is what you are building your system around, and what you might be giving up in the process.

We have been doing site selection for nearly 30 years. In that time, economic development followed a fairly predictable model: build sites, market them, and hope for the right project to show up.

That model is gone.

The AI infrastructure buildout did not just add new demand to the system. It changed the nature of the competition entirely. We have moved from attraction to allocation.

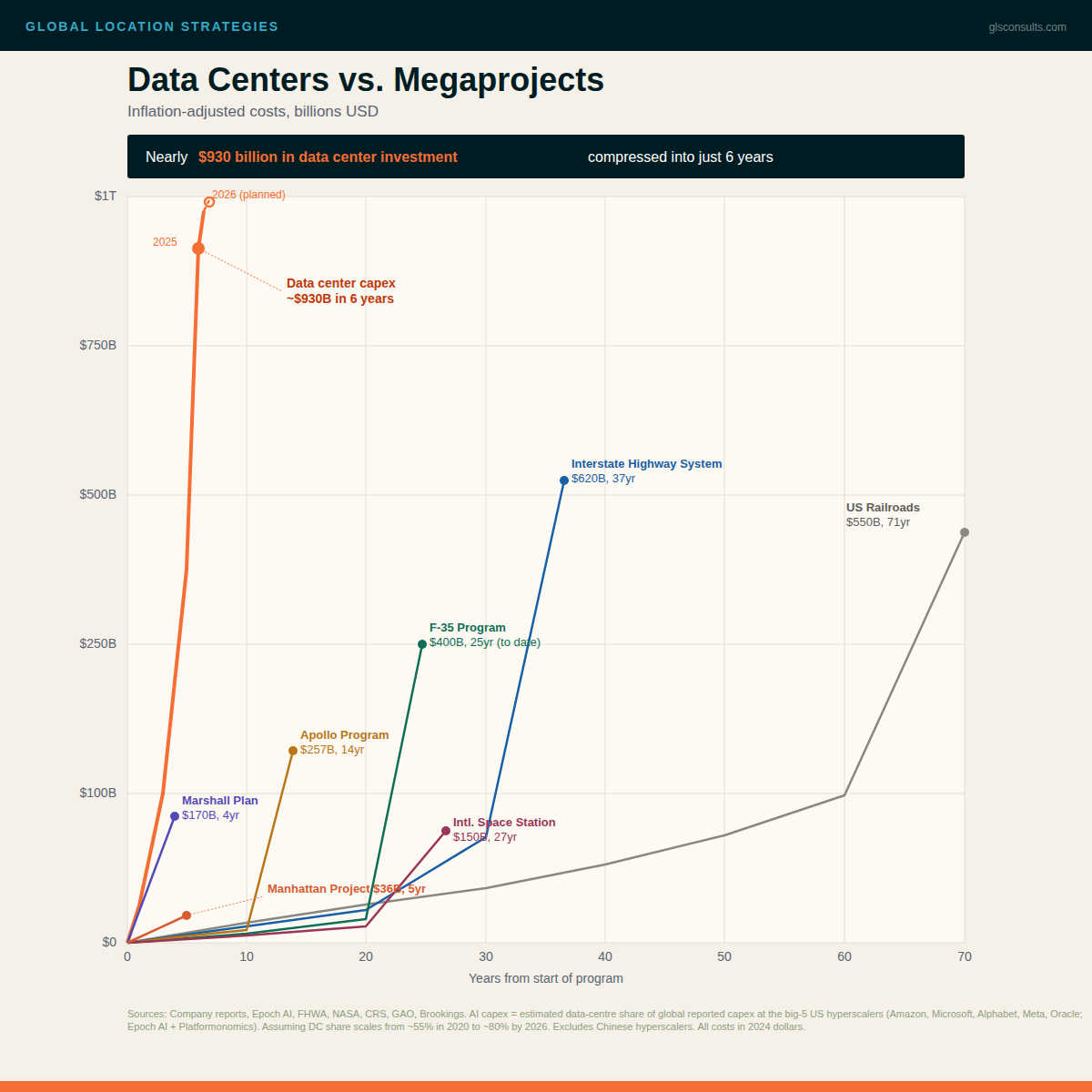

$930 Billion in Six Years: Why the AI Buildout Is Straining the U.S. Power Grid

To understand why, start with the scale of what is happening. Data center capital expenditure is approaching $930 billion in just six years.

To put that in context, the Interstate Highway System cost $620 billion over 37 years. The Apollo Program cost $257 billion over 14 years. The U.S. railroad network cost $550 billion over 71 years. We are compressing more infrastructure investment into a shorter period than anything in modern history.

Sources: Company reports, Epoch AI, FHWA, NASA, CRS, GAO, Brookings. AI capex = estimated data-centre share of global reported capex at the big-5 US hyperscalers (Amazon, Microsoft, Alphabet, Meta, Oracle; Epoch AI + Platformonomics). Assuming DC share scales from ~55% in 2020 to ~80% by 2026. Excludes Chinese hyperscalers. All costs in 2024 dollars.

This buildout is structurally different from prior cycles in four ways.

- Speed – AI demand is scaling faster than utilities can plan, permit, and build. The systems designed to absorb incremental growth are being asked to absorb step-change demand.

- Concentration – Load is clustering in a few hubs, putting extreme pressure on local grids. What used to be a large project, 100 acres, 100 jobs, $100 million in investment, and 5 megawatts of power, is now easily digestible. Today we are seeing 300, 500 megawatts, even a gigawatt of power going to a single location.

- Capital Intensity – New power and data infrastructure requires enormous upfront investment before returns arrive. The utilities and communities making these commitments are doing so before the demand they are serving is fully proven.

- Uncertainty – Demand timelines and technology shifts make every forecast harder to trust. The system was not designed to make decisions at this speed.

Three Hidden Risks Behind AI Data Center Growth

Underneath the buildout, three separate concentrations are stacking on top of each other simultaneously. The problem is not any one of them in isolation. It is their correlation.

1. Fuel

In the late 1990s, natural gas made up roughly 9 to 11 percent of U.S. electricity generation. Today it exceeds 40 percent. Natural gas is not a dispatchable fuel source the way coal historically was. There is no reserve sitting on site.

The system runs on flow, and flow is weather-dependent and pipeline-constrained. When heating demand and generation demand spike at the same time, as we saw during Winter Storm Uri and more recently during Winter Storm Finn, the margin for error collapses.

2. Demand

Hyperscale clustering is creating multi-gigawatt loads in narrow geographies. This is not diversified industrial demand that fluctuates with weather and production cycles. It is non-discretionary baseload that does not curtail.

When you add that kind of flat, inflexible load to a grid, every peak event becomes sharper and more expensive for everyone on the system.

3. Fiscal

In some communities, a single data center project can generate tax revenue that dwarfs the existing municipal budget. That sounds like a win. It can be, if the revenue is managed intentionally. But it also creates budget dependency on a single customer class in a single sector, which is exactly the kind of concentration that creates long-term vulnerability.

Concentration equals correlation. Correlation equals volatility. All three are compounding simultaneously, and most communities are planning for each one separately rather than understanding how they interact.

Two Scenarios for the AI Economy, and Why Both Create Challenges for Communities

Ten years from now, we will say one of two things. We either barely built enough infrastructure fast enough, or we built more than the economy could absorb.

Both of these futures are plausible. And the uncomfortable truth is that the infrastructure decisions being made today have to work under either one.

If demand persists, infrastructure scales under pressure. Prices rise and then stabilize as costs spread across enormous new loads. Capacity remains tight. The transition is painful for manufacturers and communities trying to compete during the build-out phase.

If demand corrects, overbuild risk emerges. Cost recovery pressure mounts. Stranded capacity accumulates. Utilities that made long-term commitments based on demand projections that did not materialize are left managing assets sized for a future that did not arrive.

The risk in either scenario is the same: a timing mismatch between infrastructure commitments and the demand those commitments were built to serve. Private capital can exit when conditions change. Utilities cannot. Communities cannot. Manufacturers operating under multi-decade cost structures cannot.

How Rising Power Costs Are Already Pricing Out Manufacturers From Key Markets

Here is where this stops being abstract.

A one cent per kilowatt hour increase in power cost on a 200 megawatt load equals roughly $17 million per year. For a data center with 200 million active users, that is approximately $0.09 per user annually. Absorbed easily. Essentially invisible.

For a manufacturer producing 200,000 units per year, that same cost increase is $88 per unit. On thin operating margins, that is not a rounding error. That is the difference between a project that works and one that does not. It is the difference between a facility that expands and one that quietly goes into cost-cutting mode instead.

Dale Rector, an energy consultant with Advantage Energy and a GLS partner with 27 years of experience in the energy sector, put it plainly during our recent webinar: industrial customers are not just failing to show up in some regions. They are failing to expand. They are in cost-cutting mode because of energy prices, and labor and new investment are the first things to be cut.

This is not a future problem. We are already seeing sites taken out of consideration. We are already seeing projects not land. Power has become the first filter, not just on availability, not just on cost, not just on reliability, but on all three combined.

Data Centers vs. Manufacturing: The Real Competition for Power, Land & Infrastructure

The shift that is underway is fundamental. Not all projects can be accommodated. Not all uses of constrained capacity are equal. Capacity must now be allocated, not simply offered.

We worked with an industrial company evaluating a site in South Carolina. The initial proposal came in at $90,000 an acre. A few weeks later, before we had even moved forward, the price had risen to $180,000 an acre. Same site, same dirt. The only thing that changed was data center interest.

That is not growth. That is competition for capacity. And it forces a different kind of decision: you cannot just take what shows up anymore.

Kenny McDonald, former President and CEO of One Columbus and founder of Little Dry Consulting, offered an important counterpoint during the webinar. In the communities where this infrastructure has been built thoughtfully, it has often catalyzed manufacturing investment rather than crowding it out.

The New Albany Business Park outside Columbus attracted early data center investment that funded transmission upgrades and skilled trades capacity. What followed was Intel, Amgen, and continued industrial investment using the same infrastructure the data centers paid to build.

The lesson is not that data centers always lead to manufacturing. The lesson is that prepared communities attract both. The difference between New Albany and a community that loses its industrial base to data center competition is strategy, utility relationships, and the institutional capacity to negotiate agreements that protect long-term optionality.

Site Readiness in the Age of AI: What Economic Developers Should be Doing Now

The moratorium some communities are reaching for is not a solution. A moratorium signals that your team is not ready to compete. Capital will move to where it can get power, get permits, and move quickly. The question is where you want to be in that story.

Here is what preparedness looks like in practice.

Work more closely with your utilities, before a project arrives.

What used to be reliable infrastructure commitments made weeks before a site visit are now multi-year planning processes involving cost allocation negotiations, regulatory approvals, and system studies. If you do not have a real-time relationship with your utility, you cannot make credible promises to prospects.

Get energy into the state-level incentive conversation, not just the utility conversation.

In the negotiation over who pays for infrastructure, communities often leave the state out entirely. The state can serve as an intermediary, helping shift and manage risk in ways that utilities alone cannot. That is a lever most economic developers are not pulling.

Understand what you are committing to before you commit.

A data center that generates revenue equivalent to dozens of manufacturing projects is genuinely transformative for a community’s fiscal position. It can stabilize or even reduce taxes for existing residents. It can fund infrastructure that catalyzes future industrial investment. But those outcomes depend entirely on how the revenue scale is introduced, negotiated, and managed. The numbers matter. So does the framework you build around them.

Control your sites.

We completed a site identification project in Missouri where the best large industrial site in the region was privately held. By the time the project was ready to move forward, the site had been sold to a data center speculator. The community lost the ability to attract investment of any kind, because the asset was in private hands waiting for a customer. When possible, control your assets.

Clarity Is Strategic

Every commitment you make right now, power, land, infrastructure, forecloses something else. Once that capacity is committed, it is very difficult to get back.

The communities and economic developers that will be best positioned a decade from now are not the ones who said yes to every project or no to every data center. They are the ones who understood what they were choosing before they chose it, built frameworks that gave them visibility before velocity, and made decisions they could defend.

Intentionality determines outcome. That has always been true in economic development. The AI power race has simply made the stakes higher and the timeline shorter.