For much of the past decade, industrial growth in the United States has been framed as a story of opportunity. Electrification. Advanced manufacturing. Reshoring. AI. Capital is flowing. Announcements are frequent. The narrative is optimistic.

But beneath the headlines, a harder reality is emerging.

Across sectors, we are seeing projects slow, stall, or collapse not because of a lack of interest or capital but because of one fundamental constraint:

Power.

We spend our days evaluating the real-world feasibility of large, complex industrial investments and increasingly, power availability, cost, and delivery timelines have become the decisive factors in whether a project moves forward at all.

This is not a future risk. It is a present one.

A Project that Nearly Didn’t Happen

Several years ago, GLS was engaged to support a transformational industrial project — a modern aluminum smelter intended to close part of a growing domestic supply gap. The stakes were high.

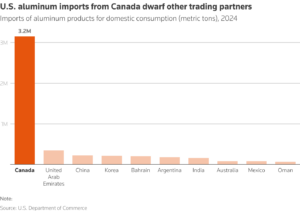

The U.S. has not built a new primary aluminum smelter in more than four decades, while domestic production has steadily declined and reliance on imports has grown.

Aluminum is foundational to defense, energy systems, transportation, construction, and other critical industries making this project strategic for the U.S.

On paper, the opportunity was compelling:

- $4 billion in capital investment

- Thousands of direct and indirect jobs

- A new regional manufacturing ecosystem

But none of it mattered without power.

This single facility would require gigawatt-scale electricity, roughly the amount needed to power an entire U.S. state. Electricity dominated the cost structure, making power availability and long-term price certainty the determining location factor.

What followed was a multi-year search across 46 states and provinces, spanning two countries. Many sites looked promising in early screenings. Far fewer survived deeper analysis.

Demand is Rising Faster than the System Was Built to Handle

The challenge we encountered is not unique to aluminum.

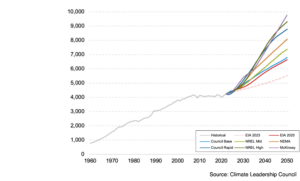

U.S. electricity demand has entered a new phase and one the existing system was not designed for. For decades, load growth was modest and predictable. Today, it is anything but.

Between 2023 and 2025, federal forecasts had to be revised upward by the equivalent of adding the combined electricity demand of Texas, California, Florida, and Ohio.

Much of that increase is driven by data centers, electrification, and advanced manufacturing.

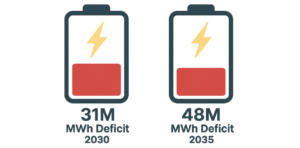

The result is a widening gap between demand and deliverable supply.

Projected U.S. Energy Deficit

Utilities across the country are warning that they cannot serve new large loads without significant upgrades. Interconnection queues are growing. Transmission constraints limit where power can be moved.

These pressures are now shaping industrial site selection outcomes in ways we have not seen before.

Industry data confirms this shift. In the Site Selectors Guild’s most recent survey, power availability ranks among the top risks impacting industrial projects.

When “Viable” Sites Collapse Under Scrutiny

For our aluminum project, once real-world conditions were layered onto site requirements (land, workforce, infrastructure, and power) the viable universe shrank quickly.

From dozens of candidate locations, we narrowed to 36 sites across 19 states and provinces that appeared technically feasible.

From there, only four warranted on-the-ground site visits.

That’s when the challenges mounted.

Utilities are increasingly implementing new rules for “large loads,” largely in response to speculative data center demand. While these rules are often reasonable in intent, their impact on manufacturers can be severe.

One site that initially showed promise ultimately became unviable when the utility required full upfront responsibility for system upgrades and significantly higher rates with little flexibility to find a workable solution.

The economics were stark.

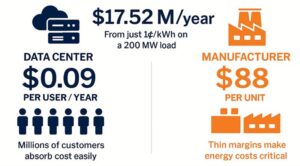

A one-cent per kilowatt-hour increase for a 200 MW load equates to roughly $17 million per year.

A hyper-scale data center can often absorb and socialize that cost across millions of users. A manufacturer selling a finite number of units cannot.

The same price increase can translate into tens of dollars per unit, wiping out already thin margins.

That cost asymmetry matters beyond the balance sheet. Data centers can enter a market, move quickly, and contract for finite available power without the same sensitivity to rate structures that manufacturers require to reach a competitive cost position. When data centers and manufacturers compete for the same scarce power, manufacturers are structurally disadvantaged.

In another case, a data center secured available power ahead of our client, effectively removing the site from consideration altogether.

What began as four viable options narrowed to two.

Deregulated Markets are Not a Panacea

Our prioritized sites happened to be in regulated electricity markets. As these options tightened, we paused to revisit deregulated territories in search of more creative flexible solutions. But here too, constraints emerged.

In ERCOT, the deregulated grid in Texas, large-load queues have quadrupled in a single year. Interconnection wait times for new generation nationally now approach five years.

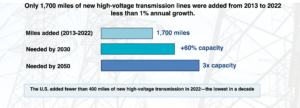

And in addition to these challenges, deregulated markets still faced the same transmission constraints we were seeing nationally. According to Lawrence Berkeley National Laboratory, transmission capacity is lagging far behind what reliability and clean energy goals require with less than 1% annual growth in high-voltage lines over the past decade.

The lesson was clear: there is no “easy” market for gigawatt-scale power today.

What Ultimately Made the Project Viable

In the end, the solution was not another market. It was a return to fundamentals.

This project moved forward only because of:

- Deep partnership across utilities, state, and local leaders

- Political will to prioritize industrial power needs

- A holistic approach leveraging infrastructure, incentives, policy, and timing

The project was announced in 2025, with a multi-year buildout that aligns power delivery with construction and permitting timelines. Had the search begun even a year later, the outcome might have been very different.

And our experience is not an outlier.

This is Better than Economic Development

Across the country, power-intensive projects are facing the same constraints. Reliable, affordable electricity has become the limiting factor for reindustrialization.

This is not simply an economic development challenge. It is a competitiveness and national security issue.

In just three strategically critical sectors: critical minerals, defense manufacturing, and advanced manufacturing, the new industrial load required to meet domestic demand will be substantial. The grid, as currently built, is not positioned to deliver it.

If we cannot deliver that power, we risk slowing reindustrialization, raising costs for consumers, and falling behind in technologies that matter.

Powering the Next Era Requires Alignment

The question cannot be whether power-intensive projects are still viable in the United States. To meet our national priorities and to remain globally competitive, they must be. But success now requires intentional coordination.

No single solution is sufficient on its own. What’s required is alignment across:

- Transmission and permitting reform as a foundation

- An all-of-the-above generation strategy

- On-site and distributed solutions to manage risk and resilience

These tools only work when deployed together.

The locations and projects that succeed will be those grounded in delivery realism: clear-eyed about constraints, honest about trade-offs, and disciplined in execution.

That is the work ahead.